August CPI inflation data was worse than expectated and the markets repriced in response. Bitcoin falls more than 10% and the S&P 500 closes down 4.3%.

The below is an excerpt from a recent edition of Bitcoin Magazine Pro, Bitcoin Magazine’s premium markets newsletter. To be among the first to receive these insights and other on-chain bitcoin market analysis straight to your inbox, subscribe now.

Inflation Is Not Over

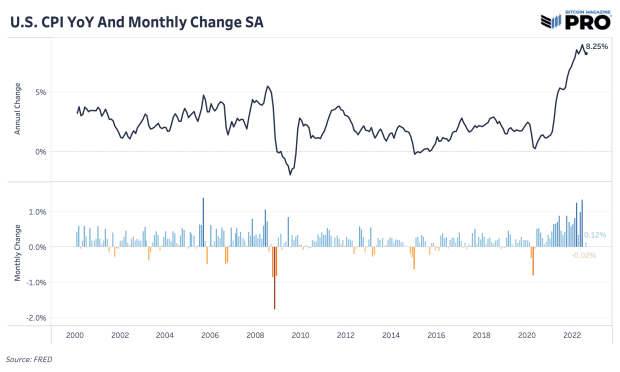

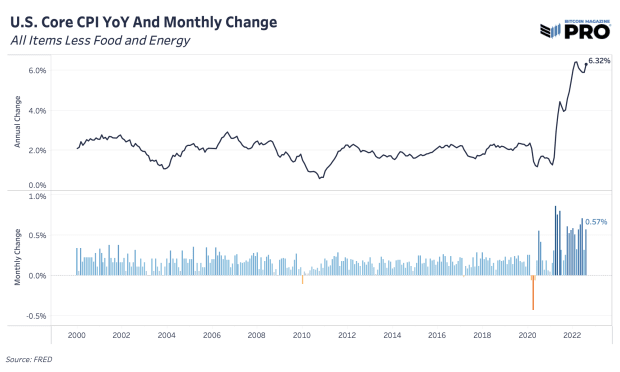

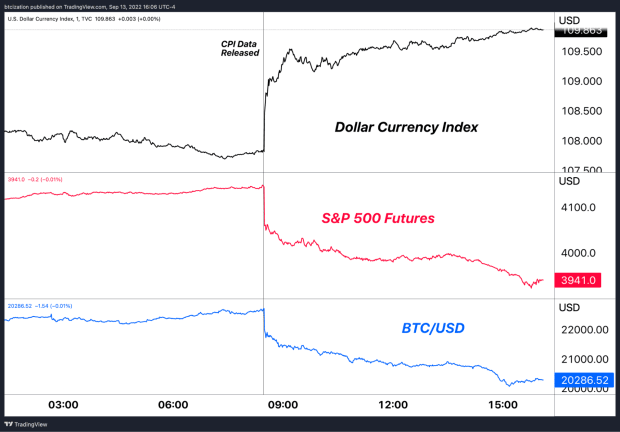

Despite the overall consensus and sentiment for good inflation news this past month, the higher-than-expected U.S. August Consumer Price Index (CPI) print has derailed any short-term bullish momentum for risk assets that’s been building over the last week. As a result, equities, bitcoin and credit yields exploded with some volatility today. The S&P 500 Index closed down 4.3% with bitcoin following on a 10% plus down move. The last time this occurred for equities was June 2020.

It’s a similar event to what we saw last month for July data, but in reverse and with more magnitude. Markets cheered on a loosely confirming trend of peak inflation last month, only to have today’s data say otherwise. Now we look to the broader market for risk and rates over the next few days to confirm this new rally downtrend or some relief with the Merge expected to take place late tomorrow night.

Both headline CPI and Core CPI beat expectations that had consensus positioning for month-over-month deceleration. Instead, we got both headline CPI and Core CPI rising month-over-month to 0.12% and 0.57% respectively. In simpler terms, inflation has not been vanquished yet and there’s more work to do (or attempt to do) on the monetary policy front. The Cleveland Fed Inflation Nowcast pretty much nailed their August forecast.

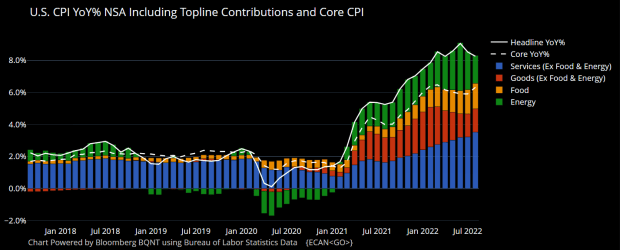

Although we did see some inflation across energy commodities come down, it wasn’t enough to offset the growing inflation in the services sector. Higher and elevated wage inflation remains a key, sticky part of inflation that is yet to come down. Housing inflation is also still an issue and has yet to come down. Housing inflation and prices have typically been the last to fall into a pending deflationary and/or recessionary period. Rent inflation (aka owners’ equivalent rent (OER)) is a significant component that can keep up CPI prints for longer as it’s usually a six-to-nine-month lag.

Overall, the inflation picture looks to be sticky and broadening. Based on the Federal Reserve’s statements over the last few months, it’s a clear sign to keep aggressive monetary policy via rate hikes going.

Immediately following the release of the CPI data, equities and bitcoin began to sell and the dollar soared. The price action of the asset classes was less about the inflation itself and more about the market’s expectations for future monetary policy from the Federal Reserve.

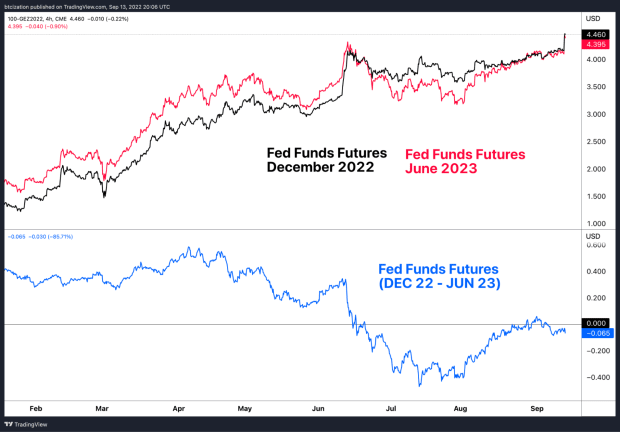

Expectations for rates immediately jumped to new yearly highs, with the market now pricing in a Fed Funds rate of 4.46% for December of this year, which is almost 200 basis points less than the current rate target rate range of 2.25-2.50%.

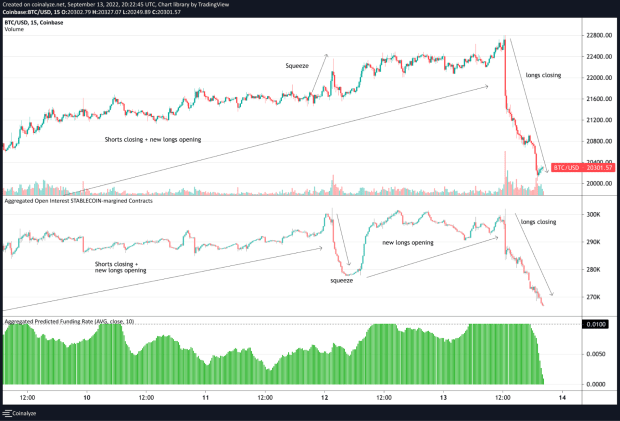

Bitcoin in particular was subject to a large unwind in open interest as traders speculating on peak inflation by going long futures now were underwater en masse.

The decline in stablecoin margin open interest was greater than 30,000 bitcoin from the release of CPI data to the close of legacy markets. Assuming the majority of the decline in open interest was longs closing positions, the market faced the equivalent of approximately 25% of MicroStrategy’s bitcoin stash in selling pressure in the course of a few hours.

With that said, we are as convicted as ever in an ultimate capitulation moment having yet to occur across global financial markets. Long-term investors shouldn’t fear downside volatility, but rather embrace it, understanding the unique opportunity it provides to buy high quality assets at fire sale prices.