The funding rate is a key mechanism in Bitcoin perpetual futures designed to keep the contract price as close as possible to BTC‘s spot price. It’s a periodic payment exchange between long and short traders, determined by the difference between the perpetual futures and spot prices. When the funding rate is positive, long positions pay shorts; when it’s negative, shorts pay longs.

Monitoring the funding rate is crucial for analyzing the market as it’s one of the best indicators of trader positioning, particularly in leveraged trading environments. A consistently high or positive funding rate indicates a bullish sentiment, as more traders are willing to pay a premium to hold long positions in a perpetual contract. Conversely, a negative funding rate shows a bearish sentiment, with traders more inclined to short the asset and, in turn, pay a premium.

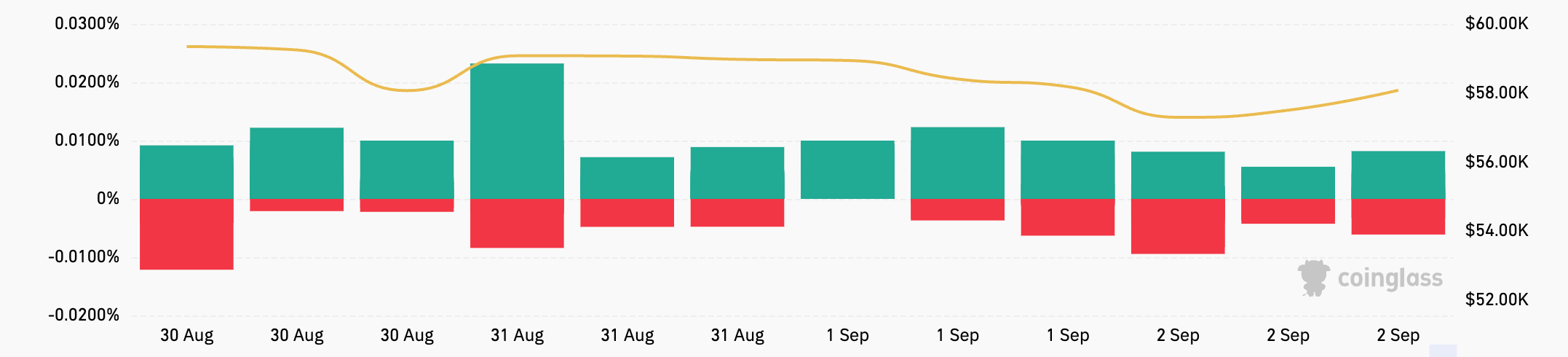

Throughout the weekend, the funding rates for USDT and USD-margined contracts fluctuated across exchanges. On Aug. 31, the rates were predominantly positive, showing a bullish sentiment, though varying in magnitude. Bitmex had the highest funding rate at 0.0089%, while OKX had the lowest at 0.0029%. On Sep. 1, there’s been a notable shift, particularly on Binance and Bybit, where the rates turned negative at -0.0004% and -0.0009%, respectively. This showed an increase in bearish sentiment on those exchanges.

This trend continued on Sep. 2 and became more pronounced on Bybit and OKX, with both platforms seeing negative funding rates of -0.0040%, indicating growing pressure from short positions. In contrast, Bitmex, which had the highest funding rate on Aug. 31, saw a significant drop to 0.0048% by Sep. 2, though it remained positive. HTX‘s funding rate also decreased but stayed positive at 0.0014%. Funding rates vary so much across exchanges due to the differences in trader sentiment and positioning on each platform, which are most likely influenced by liquidity, trading volume, and the specific trader base.

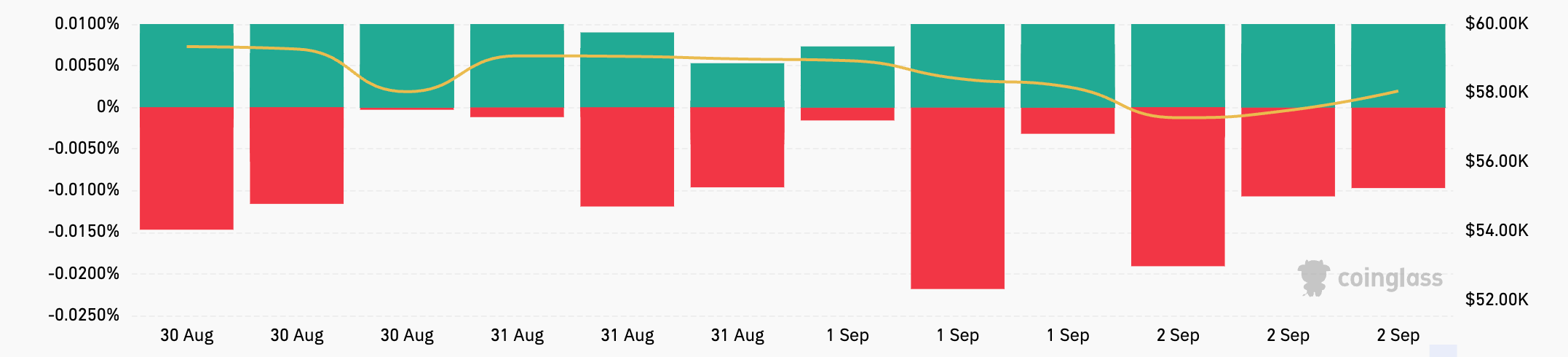

The funding rates for token-margined contracts during the same period were much different. By Sep. 1, most exchanges saw negative funding rates, with Bybit and OKX dropping to -0.0096% and -0.0044%, respectively. On Sep. 2, the divergence became more pronounced, with Bybit’s rate falling to -0.0191%, suggesting intense bearish pressure, while HTX saw a significant jump to 0.0100%, indicating a sharp reversal in sentiment on that platform.

This disparity in funding rates between USDT/USD-margined and token-margined contracts shows how traders in these markets behave differently.

USDT and USD-margined contracts, settled in stablecoins and fiat, are generally preferred by traders who want to avoid exposure to Bitcoin’s price volatility when settling profits and losses. These contracts are popular among retail traders and those who use leverage to take directional bets on Bitcoin’s price movement without affecting their underlying Bitcoin holdings.

On the other hand, token-margined contracts are settled in BTC or other cryptocurrencies, making them more appealing to traders with a long-term bullish view of Bitcoin or comfortable with the inherent risk of additional volatility. These contracts are often used by more sophisticated traders or those with a long-term holding strategy, as they offer the potential for more significant gains and greater risks due to their exposure to Bitcoin’s price.

The differences in funding rates between these two types of contracts during this period show the traders’ varying risk appetites and strategies. The negative funding rates for token-margined contracts indicate that traders in these markets were more bearish or risk-averse, possibly anticipating further Bitcoin price declines.

In contrast, the generally more stable and positive funding rates for USDT/USD-margined contracts suggest that traders in these markets were either more bullish or less concerned about short-term price volatility.

It’s also important to analyze these changes in funding rates alongside Bitcoin price fluctuations. During the weekend, Bitcoin’s price declined from $58,970 to $57,570 — a relatively modest drop in the context of Bitcoin’s historical volatility. However, the sharp swings in funding rates, particularly the negative shifts on Binance and Bybit for USDT/USD-margined contracts and the extreme negativity in token-margined contracts, suggest that traders were increasingly positioning for further downside risk.

The overall decline in the volume-weighted funding rate from 0.0050% on Aug. 31 to -0.0017% on Sep. 2 shows how sharp this shift in sentiment was, as traders increasingly took short positions or reduced their exposure to long positions.

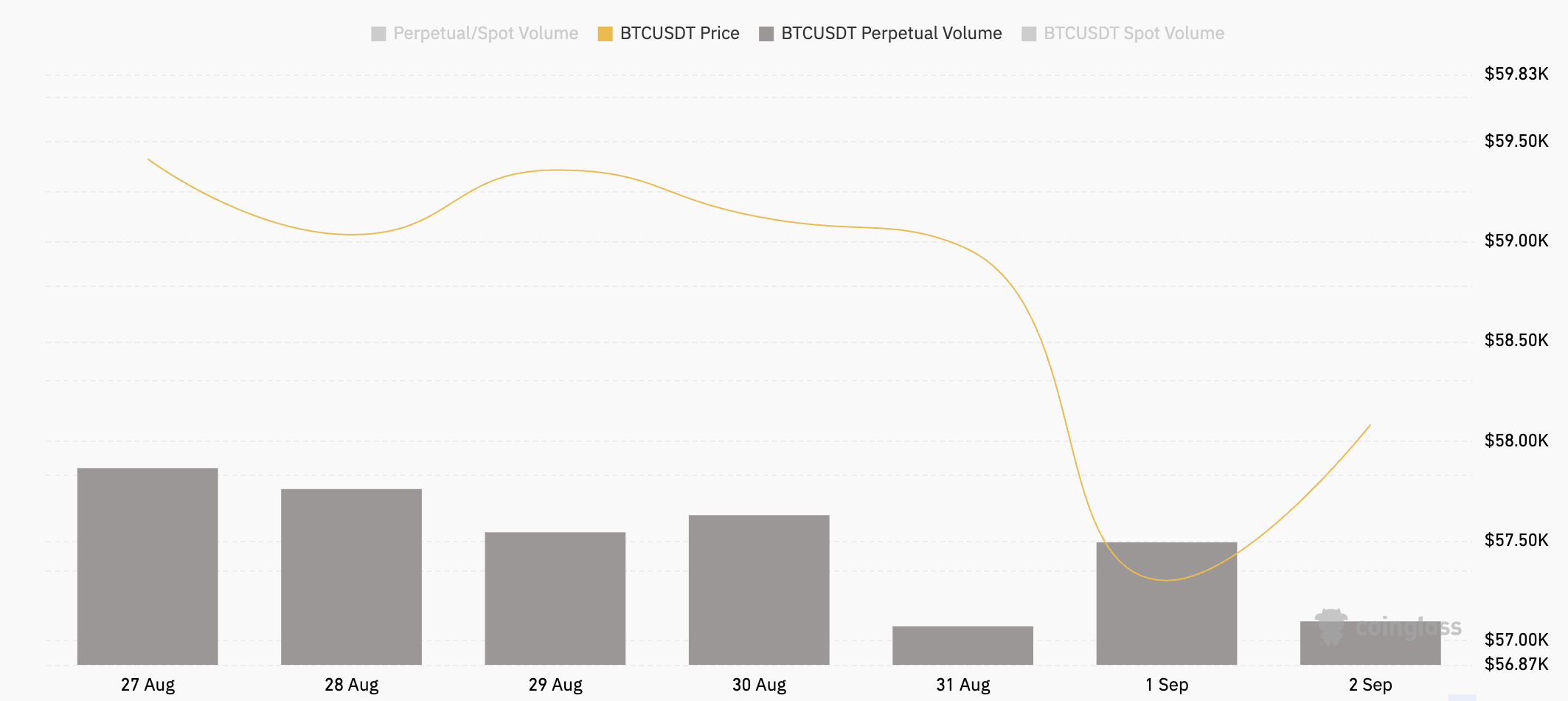

Perpetual futures trading volume also fluctuated significantly throughout the weekend, seeing a sharp drop on Aug. 31 and Sep. 2, contrasted with higher volumes on Sep. 1. This suggests that traders were either taking profits or cutting losses amid market uncertainty, leading to a decline in OI and trading activity as the funding rates began to shift.

The post Bitcoin funding rate volatility shows market-wide caution appeared first on CryptoSlate.

{kind=link}